Fixed-Rate Increases Costing Today’s Homebuyers Over $10,000 More in Interest

Fixed mortgage rates have been climbing steadily since September. But by how much and at what cost to new homebuyers?

We’re about to answer that. But first, let’s look at what’s been driving rates higher.

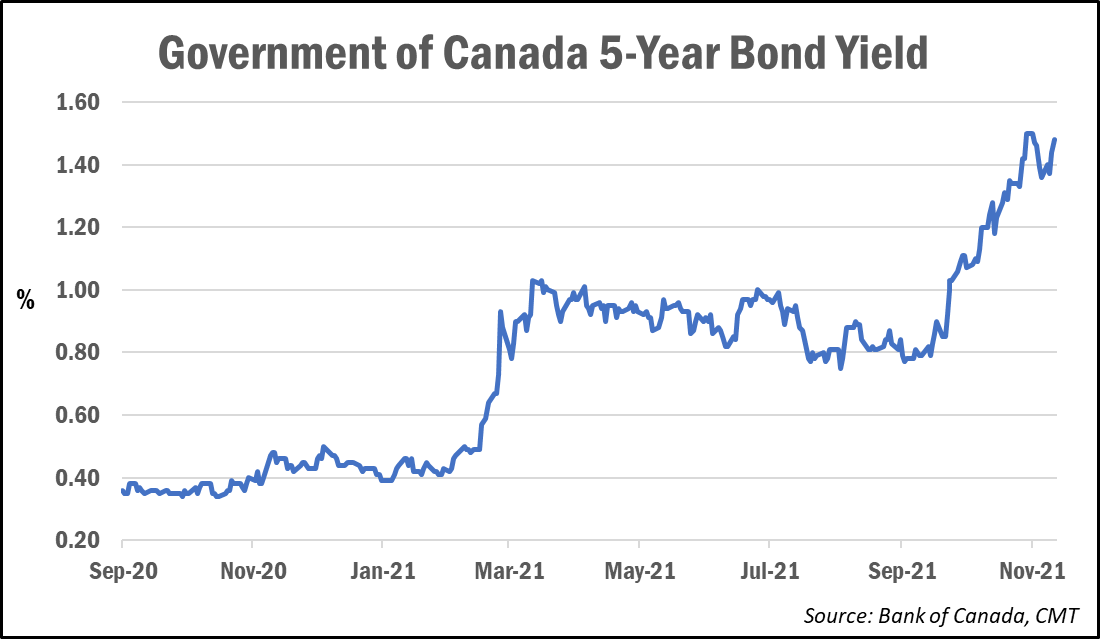

After a short-lived spike in rates earlier in the year, fixed mortgage rates have spent most of 2021 going sideways, just off their all-time lows reached in December 2020.

They got a second-wind in late September, soon after bond yields started shooting upwards. As the chart below illustrates, the 5-year Government of Canada bond yield, which leads fixed mortgage rates, took two steps higher during both those periods.

Bond yields started to rise in September at the first hint of hawkish sentiment from the Bank of Canada. This included signals that the Bank would end its bond-buying program (Quantitative Easing), which had been in place throughout the pandemic to add liquidity to financial markets, and guidance that interest rates would start to rise sooner than expected in 2022 (among other economic indicators).

Within days of the 5-year bond yield reaching multi-month highs, mortgage lenders started to raise rates.

Here’s a look at the default-insured 5-year fixed rates that were available as of October 1 vs. today from some of the big banks and key mortgage lenders (meaning rates available for mortgages with a down payment of less than 20%):

| As of Oct. 1, 2021 | As of Nov. 11, 2021 | Difference | |

| RBC | 2.19% | 2.94% | +75 bps |

| TD | 2.19% | 2.64% | +45 bps |

| Scotiabank (eHOME) | 1.99% | 2.48% | +49 bps |

| National Bank | 2.19% | 2.69% | +50 bps |

| Desjardins | 2.24% | 2.79% | +55 bps |

| First National | 2.19% | 2.69% | +50 bps |

| Equitable Bank | 2.19% | 2.54% | +35 bps |

| Average Rate Increase | +51 bps |

So, in tangible terms, what does a 50-basis-point increase translate into for today’s homebuyers?

Based on the average new mortgage amount of $450,000, according to CIBC, and an assumed Oct. 1 rate of 2.19% and a Nov. 11 rate of 2.69%, today’s homebuyers would be paying an extra $112 in monthly mortgage payments, translating into about $10,549 extra in interest over the five-year term.

Keep in mind that savvy shoppers could find even lower rates from certain brokers and brokerages.

Variable Rate Hikes to Start Next Year

Meanwhile, variable rates on new mortgages had been falling over the last several months, but that trend appears to have ended, with some lenders slowly hiking their variable rates in anticipation of coming Bank of Canada rate hikes.

Variable rates are priced based on a lender’s prime rate, which takes its direction from the Bank of Canada’s overnight target rate, which is currently still at an all-time low of 0.25%. But the Bank of Canada has indicated it expects to start hiking rates by the “middle quarters” of 2022.

Current market forecasts show the Bank of Canada on track for seven quarter-point (25 bps) rate hikes by the end of 2023, with Scotiabank expecting eight rate hikes.

Rate Cuts Already on the Horizon

But with such a rapid pace of hikes forecast, Overnight Index Swap (OIS) markets are already foreseeing a need to lower rates once again by 2024.

“Implied pricing in the bond market shows Canadian rates peaking after just two years, and then falling slightly in 2024,” noted rate observer Rob McLister in a recent Globe and Mail column. “Mortgage shoppers can’t rely on that, unfortunately. It’s just a projection that will undoubtedly change. But it does reinforce how bond traders believe that rate hikes won’t last.”

CIBC’s Benjamin Tal said higher interest rates will also start to impact the housing market, leading to reduced demand for new and existing units.

“Current variable-rate holders might choose to keep their principal payments untouched, and thus will absorb the full impact of higher rates—potentially at the expense of other spending,” he wrote.

Meanwhile, recent fixed-rate mortgage holders won’t see any impact from higher rates until their renewals come due in the years ahead.

“Despite the protection enjoyed by existing mortgage holders, higher rates will still be effective in slowing economic activity,” Tal added. “Moving too fast, as the market suggests now, is therefore inadvisable.”

Sleep Easy Financial has access to 90+ mortgage lenders including the big banks. We beat the banks’ mortgages and our services are at no cost to you as we get paid by the lenders. Whether it’s for your next home purchase, mortgage renewal or refinance, our licensed mortgage professionals are committed to getting you your lowest rate so you save as much money as possible. We help you at every stage of the journey and are with you for the life of your mortgage. Be mortgage savvy and let us shop your next mortgage for you. Contact us or schedule your complimentary consultation today.

Sleep Easy Financial mortgage and home financing services are available across Mississauga, Brampton, Cooksville, Malton, Etobicoke, Scarborough, East York, North York, Toronto, Hamilton, Milton, Markham, Woodbridge, Vaughan, Ajax, Pickering, Kitchener, Richmond Hill, Whitby, Oshawa, Guelph, and the surrounding areas. Visit our website at www.sleepeasyfinancial.ca to learn more.

Original Article Source Credits: Canadian Mortgage Trends, https://www.canadianmortgagetrends.com

Article Written By: Steve Huebl

Original Article Posted on: November 11

Link to Original Article: https://www.canadianmortgagetrends.com/2021/11/fixed-rate-increases-costing-todays-homebuyers-over-10000-more-in-interest/