All home buyers and sellers look forward to the day of closing - the day where all involved parties finalize the sale of the real estate property and the keys are finally exchanged over to the excited new owners.

The closing is by nature the most complicated step of the home buying and selling process. It consists of tying together all loose ends and officially sealing the deal. We'll take a closer look at each step of the real estate closing process and provide a few helpful tips for both homebuyers and sellers.

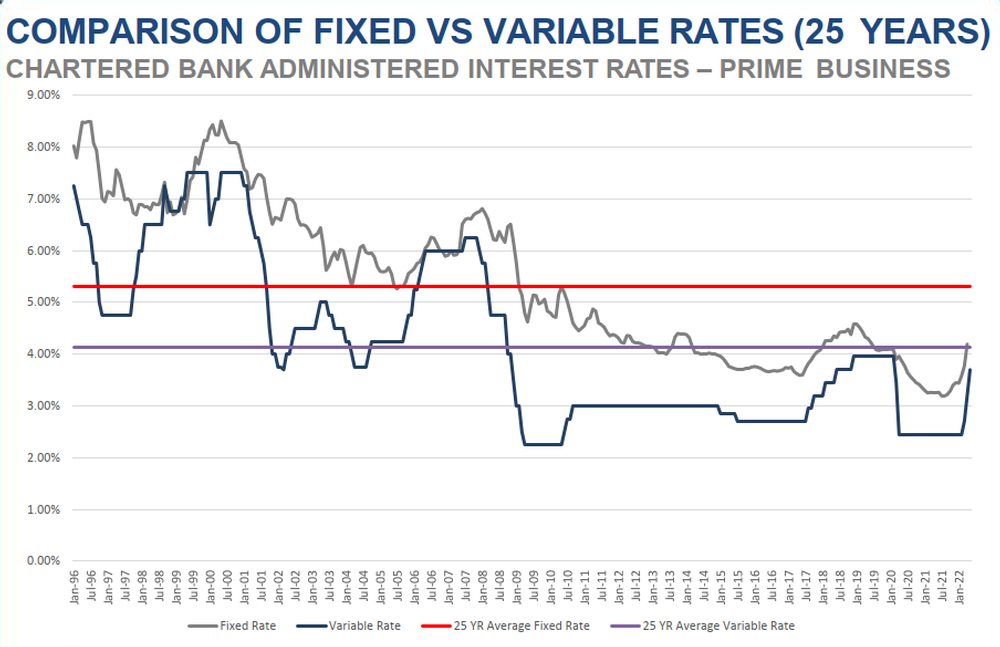

To fix your mortgage rate or not to fix? That is just one of the questions facing people looking for the best mortgage deal right now in an economy marked by the slings and arrows of inflation and climbing interest rates.

Whether it’s a new mortgage or a renewal, buyers and homeowners are filled with questions: What’s the best rate? Does locking in make sense while interest rates keep rising? If I lock in, for how long?

Canadians have seen interest rates rise considerably this year and those not on a fixed interest rate mortgage have seen their regular mortgage payments rise along with them. All the talk in the media, and rightfully so, is about the rise in mortgage payments, but what often gets overlooked is the longer-term impact to your financial health and retirement savings.

We have all heard stories about mortgage payments rising by $1,000 per month, but what about the impact of higher interest rates to service a mortgage over its lifetime?

Canada’s mortgage stress test applies to anyone applying for or renewing a home loan through a federally regulated lender.

And apparently nearly half of Canadians (according to a poll conducted by TD Bank) don’t understand what the test is—or who it affects. Here’s your primer on the mortgage stress test!

With the many increases to Mortgage Rates recently, mortgage borrowers are finding they are qualifying for lower mortgage amounts than they were just one month ago. This is true even in the absence of any change to the rate used by the dreaded Mortgage Stress Test.

The Bank of Canada released a new study where, for the first time, it classified homebuyers into three distinct groups: first-time buyers, repeat buyers, and investors.

Whether it is your first house or you’re moving to a new neighborhood, getting approved for a mortgage is exciting! However, even if you have been approved and are simply waiting to close, there are still some things to keep in mind to ensure your efforts are successful.

To avoid having your mortgage approval status reversed or jeopardizing your financing, be sure to stay away from these 10 common mortgage mistakes.

Twenty-five or thirty years can sound like an impossibly long time to service a loan – and for many of us, it is. If you are looking to pay off your mortgage faster, here are some tried-and-true tactics to get you to financial freedom that much sooner!

How much do you really know about reverse mortgages? Maybe you know that reverse mortgages can help Canadians 55+ access the equity in their home, tax-free. Maybe you know that tens of thousands of Canadians are using a reverse mortgage as part of their financial plan. But did you know that there are 7 common misconceptions when it comes to understanding reverse mortgages in Canada.

Common Misconceptions About Reverse Mortgages

1. If you have a reverse mortgage, you no longer own your home

Nothing could be further from the truth. You always maintain title, ownership and control of your home – the lender simply…